ACV vs. RCV: What Texas Homeowners Need to Know About Roof Insurance Coverage

ACV vs. RCV Roof Insurance Coverage Explained

If you’re filing a roof insurance claim in Texas, understanding ACV vs. RCV coverage can make a major difference in what your insurance company pays.

Many homeowners don’t realize they may have Actual Cash Value (ACV) coverage instead of Replacement Cost Value (RCV) coverage until they file a claim and by then, the financial difference can be significant.

Here’s what you need to know.

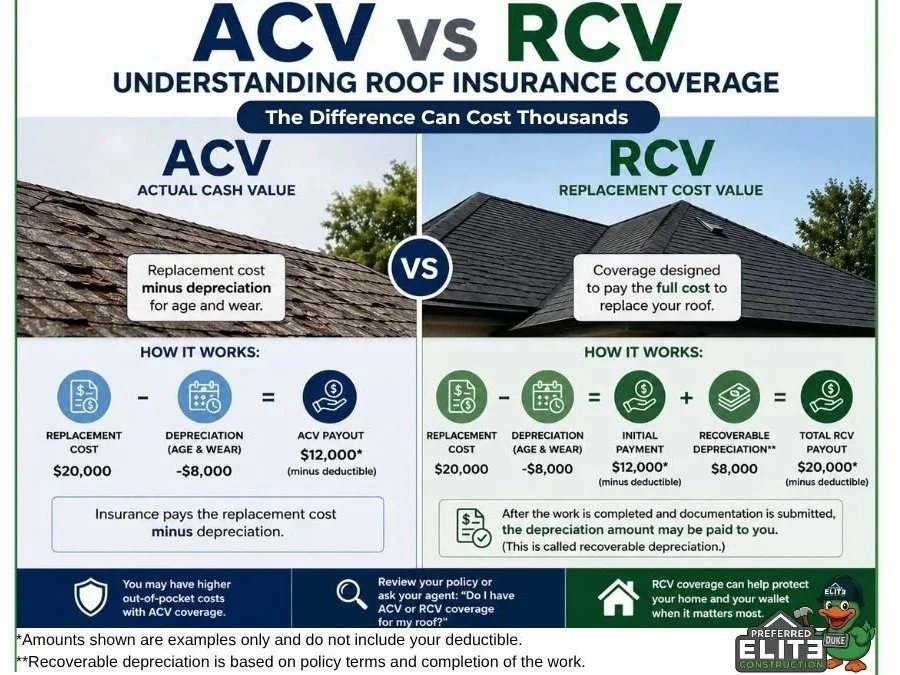

What Is ACV Coverage?

ACV (Actual Cash Value) Replacement cost less depreciation for age and wear.

In simple terms:

Replacement Cost – Depreciation = ACV Payout

If your roof is older, depreciation may reduce what the insurance carrier pays.

Example:

If your new roof replacement costs $20,000

Your 15-year-old roof has $8,000 in depreciation

With ACV coverage, insurance may pay roughly:

$12,000 (minus deductible)

The remaining difference may be your responsibility.

What Is RCV Coverage?

RCV (Replacement Cost Value) coverage designed to pay the full costs to replace your roof with similar materials at today’s pricing, subject to your policy terms and deductible.

With many RCV policies:

Insurance may issue an initial payment

Depreciation may be recoverable after work is completed

Once documentation is submitted, the remaining funds may be released

Example:

New roof replacement cost: $20,000

Your 15-year-old roof has $8,000 in depreciation

With RCV coverage, insurance will issue you a $12,000 initial payment (minus deductible)

Once work is completed and documentation is provided to insurance, typically your insurance company releases the recoverable depreciation…in this example that is the $8,000.

Total RCV payout is $20,000 (minus deductible)

With RCV coverage, you may receive coverage for the full replacement amount (subject to deductible and policy terms), rather than a depreciated payout.

ACV vs RCV: What’s the Difference?

ACV Coverage

Pays depreciated value

Lower premiums may be possible

Higher out-of-pocket costs after a claim

Common concern for older roofs

RCV Coverage

Pays replacement cost (subject to policy)

Better claim protection for many homeowners

Often higher premiums

May reduce unexpected claim costs

Why This Matters for Texas Roof Claims

In Texas, hail and wind claims are common.

Knowing whether your policy is ACV or RCV can affect:

Claim payouts

Out-of-pocket expenses

Whether repairs or replacement are financially practical

We always recommend homeowners review coverage before storm season.

How to Find Out If You Have ACV or RCV Coverage

Check:

Your declarations page

Coverage endorsements

Roof settlement provisions

Ask your insurance agent directly:

“Is my roof covered under Actual Cash Value or Replacement Cost Value?”

That one question can be huge.

Can You Switch From ACV to RCV?

Sometimes, yes.

Depending on roof age, condition, and carrier, some homeowners may have options to improve coverage. Talk with your insurance agent about available endorsements or policy options.

Need Help Understanding a Roof Claim?

At Preferred Elite Construction, we help homeowners understand storm damage, navigate claims, and make informed roofing decisions. If you’re unsure whether your policy is ACV or RCV or want a professional roof inspection after a storm, we’re here to help.

FAQ:

Is ACV or RCV better for roof insurance?

Many homeowners prefer RCV because it may provide stronger protection, but policy needs vary.

Does ACV cover roof replacement?

It may help pay toward replacement, but depreciation can reduce payout.

Do older roofs only qualify for ACV?

Sometimes carriers place older roofs on ACV policies, that’s why it’s important to talk to your insurance carrier and understand what policy you have.